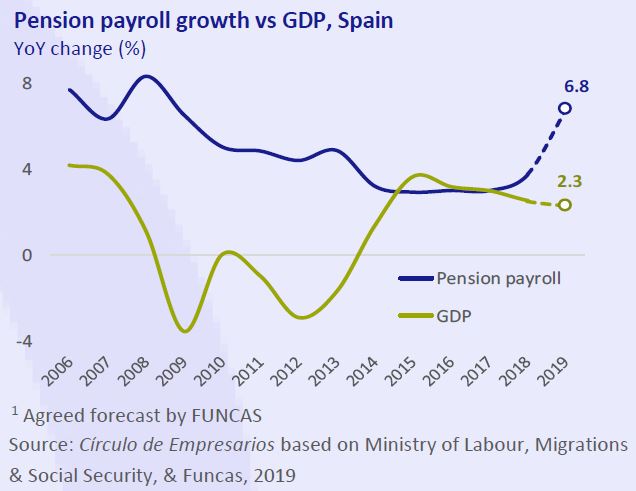

Pension expense, Spain

In August, the payroll of Social Security contributory pensions in Spain increased by 5.03% per year, reaching 9.68 billion euros per month. Between January and August, it increased at a rate of 6.8% year-on-year, compared with 3.8% in 2018 and 3% in 2017, and 4.5pp above the forecasted growth for the Spanish economy in 2019 (2.3%1). This trend places the total pension payroll at 9.8% of GDP (€116.5 billion) at the 2019 year close, which is 0.5pp higher than the total amount of 2018 (9.3% of GDP).

By type of pension, the annual progress recorded has been:

• Retirement: +5.2% (6.89 billion euros)

• Widowhood: +5.1% (1.68 billion euros)

• Permanent disability: +3.3% (939.3 million

euros)

• Orphanhood: +3.4% (138.3 million euros)

• In favour of family members: +6.2% (24.6

million euros)

Additionally, the number of pensions increased by 1.2% year-on-year in August to 9,756,142, mainly due to the increase in the number of contributory retirement pensions by 1.8% to 6,048,718 (62% of the total).

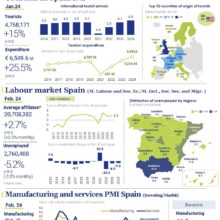

Labour market, Spain

In August, the Social Security lost 212,984 affiliates compared with July (-1.1%), reaching 19,320,227, explained by the end of the summer season and the economic slowdown. This data, the worst in 11 years, confirms the downward trend in job creation at a rate of 2.5% year-on-year, compared with 2.9% at the beginning of the year. From January to August, the number of affiliates has grown by 379,613 workers, 22% less than in the same period of 2018. Whereas, unemployment experienced the most substantial increase for August since 2010 to 3,065,804 (+54,371 people). In annual terms, unemployment fell by 3.6% (-116,264 people), 2.3pp less than in August 2018 and 5.5pp less than in the same month of 2016.

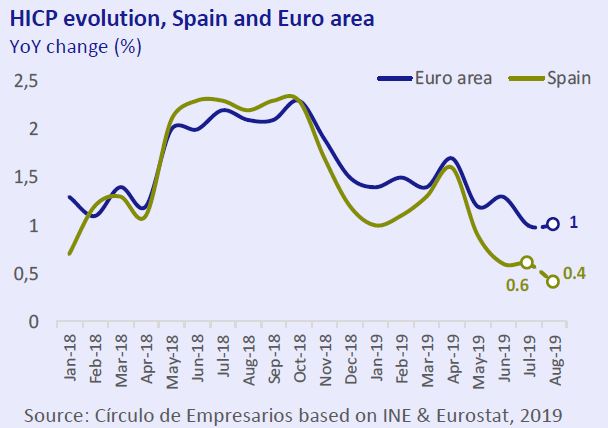

Inflation (INE), Spain

In August, the flash estimate of the HICP forecasts a change of 0.4% year-on-year in the prices of the Spanish economy, slightly lower than the 0.6% reported in the previous month, mainly due to the reduction in electricity.

If this figure is confirmed, inflation would be for the tenth consecutive month below the Euro area average (1%), which favours Spain’s competitiveness via prices in a scenario of stagnant Spanish productivity and a slowdown in the growth of the Euro area.

Germany Situation

In Q2 2019, Germany’s GDP fell by 0.1% quarter-on-quarter, after increasing by 0.4% in Q1 2019, due to the negative impact of the US-China trade war on exports and business investment, worsening of the outlook for the industrial sector, and the escalating probability of a hard Brexit.

External demand returns to contributing negatively to GDP growth (-0.5pp), with exports contracting by 1.3% quarter-onquarter, the biggest decline since 2013, slightly more than imports (-0.3%).

In domestic demand, although consumer spending remained stable, business investment moderated its progress to 1.4% quarter-on-quarter, 1 pp lower than that experienced in Q2 2018. In turn, since January, the Gross Fixed Capital Formation (GFCF) has registered an average increase of 1.7% year-on-year as opposed to the 5% average in the last 3 years. This slowdown is explained by the German companies having reduced their investments in the domestic market due to population ageing, he

shortage of skilled labour, and the stagnation of productivity in recent years.

Specifically, German labour productivity exhibits a negative evolution since Q2 2018. Currently, it is falling by 0.4% year-on-year, compared with an average growth of 0.8% in the 2013-2017 period.

Brexit

The political and institutional crisis of the United Kingdom, aggravated by the suspension of Parliament, the possibility of early elections and a probable “hard Brexit”, occurs in a context in which the prospects of the British economy worsen. In Q2 2019, the GDP of the United Kingdom registered a contraction of 0.2% quarter-onquarter, predominantly due to the decline in manufacturing production (2.3%) and construction (1.3%). As for the services sector, it experienced a marginal increase of

0.1%, its record low since 2016.

In the external sector, in June, the economy recorded its first trade surplus in 8 years, explained by a 12% fall in imports, mainly due British companies stockpiling per their Brexit contingency plans and the depreciation of the pound (5.1% since May). Likewise, in July, inflation rose to 2.1%, slightly above the 2% target of the Bank of England owing to the exchange rate effect and the increase in wages (3.9% year-onyear Q2 2019). Should this evolution persist in the medium term, then any price increases would determine the future room for manoeuvre in monetary policy.