SPAIN

National Accounts (INE)

In Q3 2017, the Spanish GDP recorded a year-on-year growth of 3.1%. It is worth noting the growth of domestic demand (2.7 points vs. 2.3 in Q2), while external demand shrank from 0.8 points in Q2 to 0.4 in Q3.

Looking at the individual components of domestic demand, the final consumption expenditure of households and the gross fixed capital formation year-on-year grew by 2.4% and 5.4% respectively.

In the foreign sector, exports of goods and services grew by 0.5%, from 4.4% to 4.9%, and imports by 1.7 points (from 2.3% to 4%).

Projected CPI (INE)

In November, the projected CPI was 1.6%, mainly due to the rise in fuel prices (diesel and gasoline). If this is confirmed, inflation will remain at the same level as that of October.

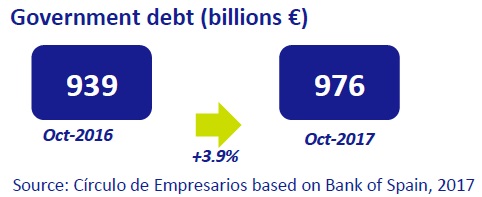

Public Debt (BdE)

In October, government debt grew by 3.9% (€36,402m), reaching €976,058m (87.2% of GDP). Of this, 84.6% corresponds to long-term debt securities (€826,032m). The remaining 15.4% is divided between short-term securities (€75,318m) and other instruments (€74,709m).

Mortgage (INE)

In September, housing mortgages grew by 9.2% year-on-year (+29,388), and the average amount borrowed was €123,649 (9.6% more than in the same period of 2016).

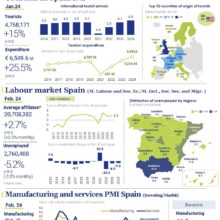

Statistical movements in borders (FRONTUR)

In October, Spain received 7.3m international tourists, with an increase of 1.8% year-on-year. The three main countries of origin were the United Kingdom with 1.6 million (+0.5% yearon- year), Germany with 1.2 million (-4.7%) and France with 800,000 (-10.2%).

The regions of Madrid and Valencia stand out, with year-on-year increases of 7.2% and 6.6% respectively, compared to Catalonia, the only one of the main tourist regions that registered a drop in foreign visitors (4.7%).

EUROPE

Macroeconomic imbalances (Comisión Europea)

In its report on Macroeconomic Imbalance Alerts, the European Commission highlights that certain significant risks and vulnerabilities persist despite the greater growth registered in the European Union, such as:

• High levels of public and private debt in Cyprus, Portugal and Greece.

• Low productivity, the fragility of the banking system and high public debt in Italy.

• The continued current account surpluses in Denmark, Sweden, the Netherlands and Germany.

• The cost of housing in Sweden, Austria, Denmark, Luxembourg, the Netherlands and the United Kingdom.

• The rise in unit labour costs in Estonia, Hungary, Latvia, Lithuania and Romania.

Inflation in the Eurozone (Eurostat)

In October, year-on-year inflation stood at 1.4% (0.1% lower than in September). By sector, the rise in fuel prices was particularly significant (+0.1%), compared to the drop in the telecommunications sector (-0.11%).

Portugal

The Portuguese economy has been experiencing a remarkable recovery since 2015:

• GDP grew by 2.5% year-on-year in 3Q 2017.

• The European Commission forecasts an unemployment rate of 8.3% by the close of 2017 (12.2% at the end of 2015).

• It is expected that by the end of 2017 the public deficit will be 1.4% of GDP (4.4% in 2015).

• In October, the harmonised CPI reached 1.9% (1.4% in Euro area).

• Since 2015, house sales have reached growth rates of around 15% year-on-year, increasing their price by an annual average of 5.3%.

Eastern Europe (Eurostat)

In Q3 2017, Eastern European economies continue to show a high level of dynamism, mainly due to higher wages and the rebound of growth in the Eurozone. The countries with the highest year-on-year growth were Romania (8.6%), the Czech Republic (5%), Poland (5%), Bulgaria (3.9%) and Hungary (3.9%).

INTERNATIONAL

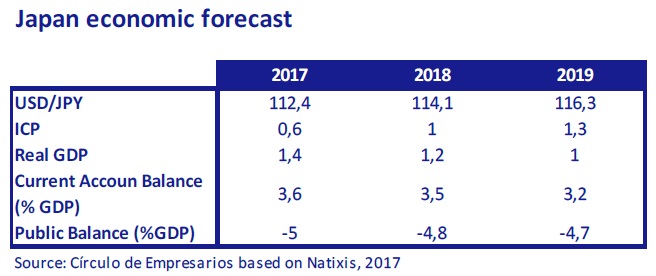

Japan

In Q3 2017, Japan’s GDP increased by 1.7% year-on-year, making it the seventh consecutive month of growth, due to improvements in the performance of exports.

USA

The US Commerce Department estimated an annual GDP growth of 3.3% in Q3 2017, supported by the upturn in public investment. With this data, the US economy returns to growth rates above 3%, which have not been seen since 2014.