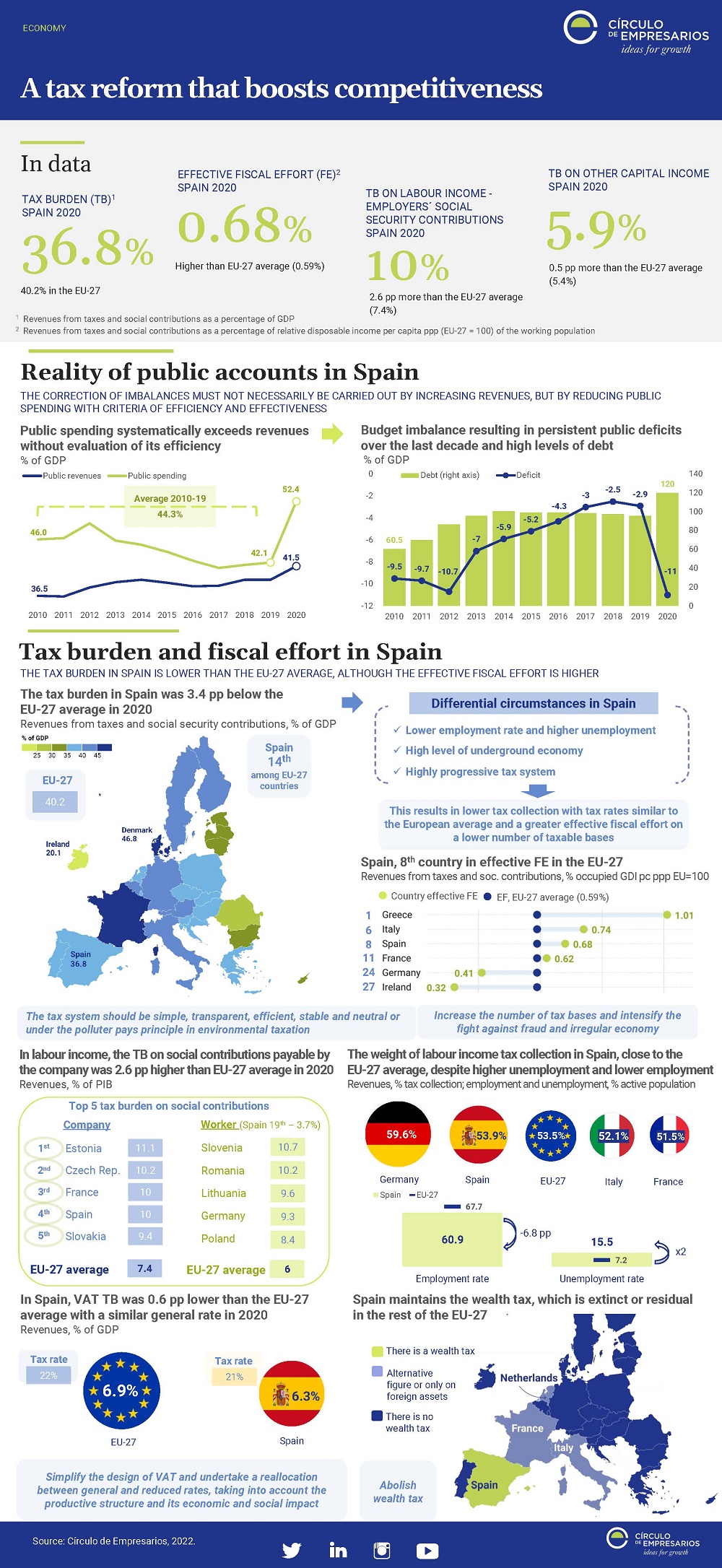

Reality of public accounts in Spain

THE CORRECTION OF IMBALANCES MUST NOT NECESSARILY BE CARRIED OUT BY INCREASING REVENUES, BUT BY REDUCING PUBLIC

SPENDING WITH CRITERIA OF EFFICIENCY AND EFFECTIVENESS

Public spending systematically exceeds revenues without evaluation of its efficiency

Budget imbalance resulting in persistent public deficits over the last decade and high levels of debt

Tax burden and fiscal effort in Spain

THE TAX BURDEN IN SPAIN IS LOWER THAN THE EU-27 AVERAGE, ALTHOUGH THE EFFECTIVE FISCAL EFFORT IS HIGHER

The tax burden in Spain was 3.4 pp below the EU-27 average in 2020

Spain, 8th country in effective FE in the EU-27

In labour income, the TB on social contributions payable by the company was 2.6 pp higher than EU-27 average in 2020

The weight of labour income tax collection in Spain, close to the EU-27 average, despite higher unemployment and lower employment

In Spain, VAT TB was 0.6 pp lower than the EU-27 average with a similar general rate in 2020

Spain maintains the wealth tax, which is extinct or residual in the rest of the EU-27