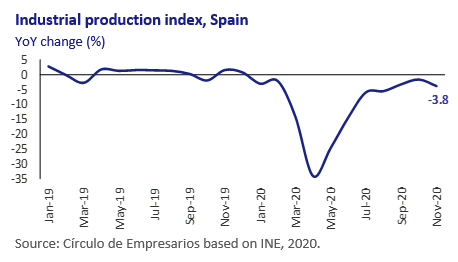

Industrial production, Spain

In November 2020, the industrial production index (IPI) fell 3.8% year-on-year against a 1.6% increase in the same month in 2019.

By sectors, all showed negative rates except intermediate goods (1.2% year-on-year). Production in the energy sector also fell 7.8% year-on-year, capital goods 7.1% and consumer goods 3.6%.

By Autonomous Community, the biggest year-on-year increases were in Extremadura (26.4%) and Murcia (4.6%). On the other hand, the Balearic Islands (-15.8%) and Navarre (-9.8%) registered the biggest decreases.

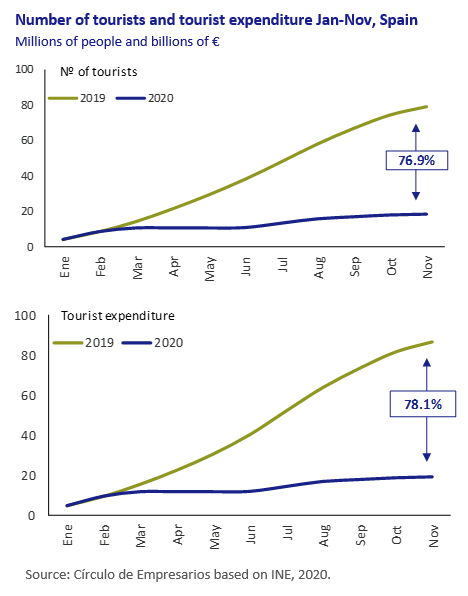

Tourism sector, Spain

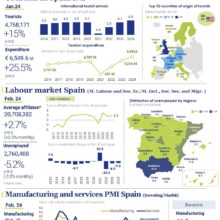

Between January and November 2020, 18.3 million tourists visited Spain, compared to 79.2 million in the same period of the previous year (-76.9% year-on-year).

By country of residence, France was the major emitter (20.3% of the total), although it registered a fall of 65% year-on-year. Next, was the UK (16.7%), with a decrease of 82.2%, and Germany (12.7%), with -78.2% year-on-year.

For its part, total spending by tourists fell 78.1% year-on-year (against +2.5% from January-November 2019), reaching €19.044 million. Average spending per person was €1,040 and the average duration of the trip was 7.7 days.

The main emitting countries in terms of spending were the UK (15.8% of the total), with a decrease of 82.3% year-on-year, Germany (13.3%), with -77.3%, and France (12.2%), with -68%.

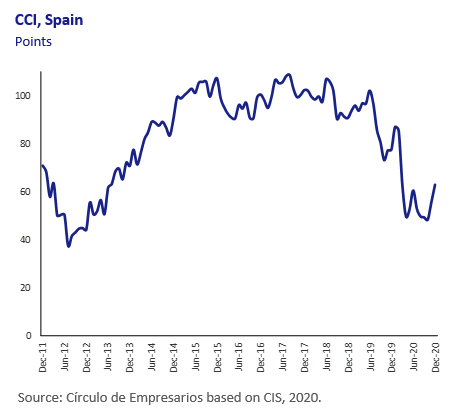

CCI, Spain

In December 2020, the Consumer Confidence Index (CCI) reached 63.1 points, compared to 55.7 points in November, and 77.7 points in December 2019. This monthly increase was due to improvements in scores for the assessment of the current situation (+4.3 points) and those related to expectations (+10.5 points). Despite the monthly upturn, this data is similar to the 2012 and 2013 values, one of the periods with the worst results since recording began. The 2020 CCI yearly average reached 59.9 points, 29.4 points lower than in 2019, making it the worst result since 2012.

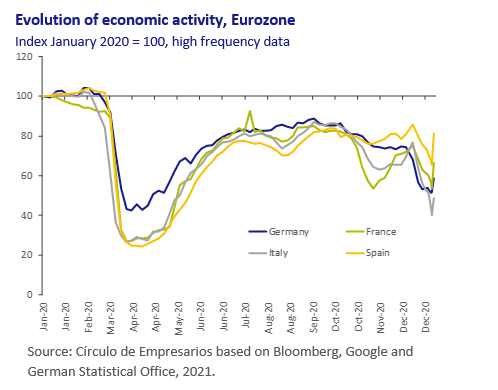

Economic activity, Eurozone

The Eurozone is heading towards a double recession as the blockages and mobility restrictions are prolonged.

Analysts from a variety of financial entities such as JPMorgan or USB Group AG arerevising their growth projections downward for Q1 2021 due to the increase in Covid-19 cases, delays in the vaccination program and the commercial disruption caused by Brexit.

In concrete, GDP growth forecast revisions for Q1 2021 are:

– Bloomberg foresees a 4% contraction against the 1.3% growth previously projected.

– JP Morgan forecasts a decrease of 1% (vs. the +2% initially estimated).

– USB is expecting a 0.4% contraction (vs. the +2.4% previously estimated).

High-frequency indicators show how mobility in retail businesses is still between 20% and 40% below the levels of January 2019.

For its part, retail sales showed a significant decrease in November of 6% monthly, while industrial production has remained stuck on +0.4% monthly since August.

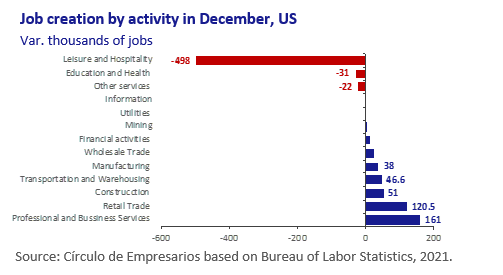

Employment, US

Employment recovery in the US has weakened due to the increase in Covid-19 cases. In December 2020, non-farm payrolls fell by 140,000 workers compared to the previous month, according to the Department of Labor. The contraction mainly occurred in restaurants, bars and other businesses affected by the new mobility restrictions.

By contrast, other labor market sectors such as retail, professional and commercial services, construction and the manufacturing sector maintained a solid rate of growth.

At the same time, the number of long-term unemployed people fell, reaching its lowest point in the past 4 months (3.37 million people).

For its part, the rate of unemployment remained at 6.7%, after a series of seven consecutive decreases.

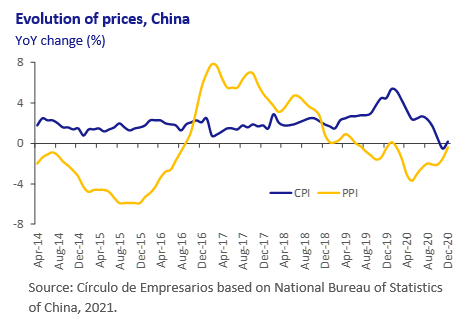

CPI, China

In December 2020, China’s CPI (consumer price index) grew 0.2% year-on-year after November’s decrease (-0,5%).

This upturn was largely due to the increase in food and energy prices. For its part, the fall in production prices (PPI) was reduced significantly to -0.4%, 1pp above the average registered for the year.