Foreclosures

In Q4 2020, foreclosures increased 109.9% year-on-year to 3,018, maintaining the upward trend which began in Q3 (+82% year-on-year).

In 2020 as a whole, after 5 years of consecutive decreases, foreclosures on main residences increased 37.4%, reaching 7,367, the biggest increase since records began in 2014.

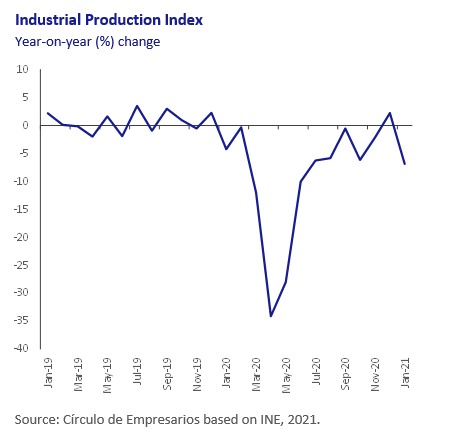

Industrial production

In January 2021, industrial production registered a year-on-year decrease of 6.9%, its biggest fall since June 2020 (-10.1% yearly). This sharp drop is related to the decreases in non-durable consumer goods (-12.2%) and capital goods (-11.2%), although the production of consumer durables (-8.8%) and intermediate goods (-5.5%) also fell. Energy was the only sector that increased production in January.

All the Autonomous Communities registered industrial production decreases, especially the Canary Islands (-15.5%), Navarre (-15%), Castile-La Mancha (-10.5%) and the Basque Country (-9.5%).

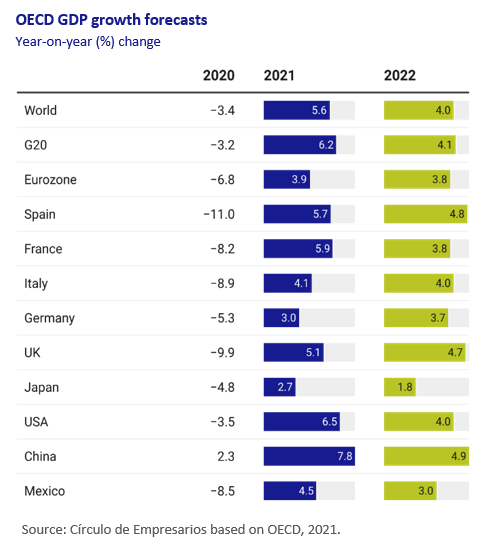

OECD forecasts for Spain

The OECD revised Spain’s GDP growth forecasts upwards against a backdrop of falling Covid-19 cases across the world, and good progress on the vaccination program.

After suffering one of the biggest economic contractions among advanced economies in 2020 (-11%), the organization forecasts annual GDP growth of 5.7% for 2021 (compared to 5% in the previous forecast), and 4.8% for 2022 (compared to 4%).

In spite of the improvement that is forecast for 2021, the increase will be 1.5pp lower than the forecast for G20 countries, and it is expected that in 2022 Spain and Italy will be the only two economies that maintain production levels below those prior to the Covid-19 crisis.

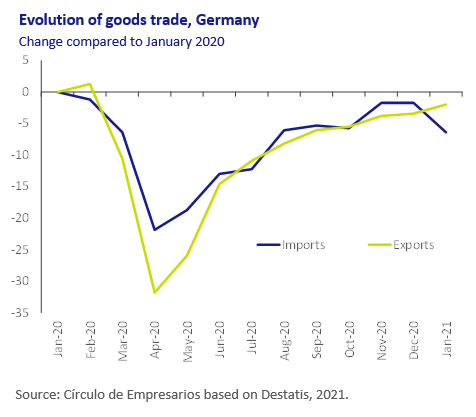

Trade balance, Germany

In January 2021, Germany’s goods trade balance improved with a monthly upturn of 35.4%, to €22.2 billion in seasonally-and working-day-adjusted terms. Exports grew 1.5%, reaching €108.8 billion, and imports fell 4.7% (to €86.5 billion).

The fall in imports reflects a deterioration in German consumption, hampered in part by the health-related mobility restrictions. In fact, in year-on-year terms, German imports are 6.4% below the January 2020 levels.

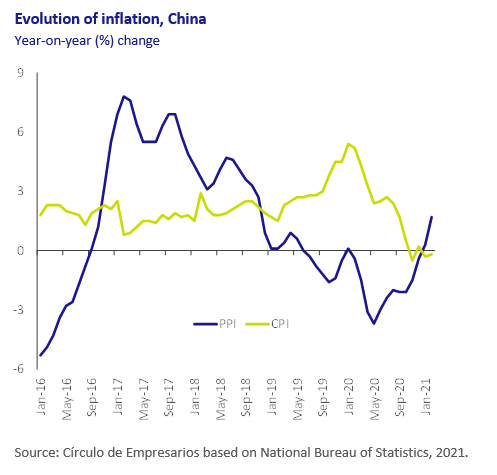

Inflation, China

In February, China’s producer price index (PPI) increased 1.7% yearly, exceeding expectations that had projected a 1.5% increase. This upturn, due in part to the inflationary pressures of oil and the scarcity of some products, could have a significant impact on global chains of production as producers pass the increase in prices onto the finished goods. For its part, the CPI stalled at -0.2% yearly, maintaining the trend from previous months.

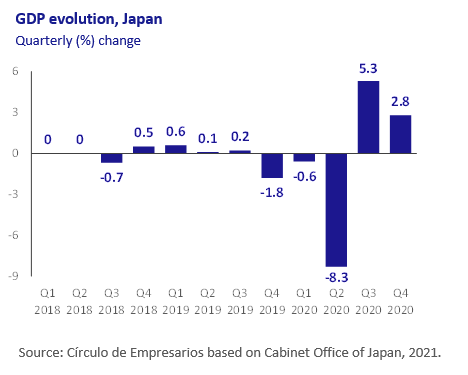

GDP, Japan

The Japanese economy is recovering as the number of Covid-19 cases decreases and vaccinations increase. In Q4 2020, Japan’s GDP increased 2.8% quarterly, a figure below preliminary estimates that pointed to a 3% increase.

Among the demand components, the increase in capital investments and private consumption stand out, with quarterly increases of 4.3% and 2.2% respectively. These figures are within the framework of a period in which the state of emergency affected two thirds of the prefectures in the country, with a significant impact on economic activity.

Within this context, the Japanese government passed a new package of direct assistance in December, with a total value of $708 billion (equivalent to 14.2% of its GDP).