SPAIN

GDP flash estimate Q3 2017 (INE)

In Q3 2017 the Spanish economy grew by 0.8% quarter-on-quarter (in comparison with 0.9% in Q2) and by 3.1% year-on-year, due to the increase

in private consumption and investment, especially in the construction sector. The foreign sector gained momentum in a global environment with a more synchronized growth.

Impact of Catalonia on growth

The Bank of Spain is warning that, if the political tensions in Catalonia continue, the Spanish economy could lose between 0.3 and 2.5 points of GDP over the next 2 years (between €3,000m and €27,000m).

In turn, BBVA Research estimates an impact between 0.2 and 1.1 points in 2018 (between €2,000m and €12,000m), reducing its growth forecasts from 2.8% to 2.5%.

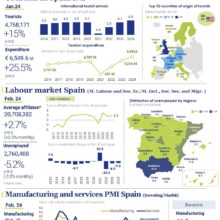

Labour market

Employed Population Survey Q3 (INE)

In Q3 2017, in annual terms, the number of those in employment increased by 2.82% (521,700 people) to 19,049,200 (from September: ▲= 94,368). 89% of the increase was recorded in the private sector. Employment grew by 502,000, 60% with permanent contracts.

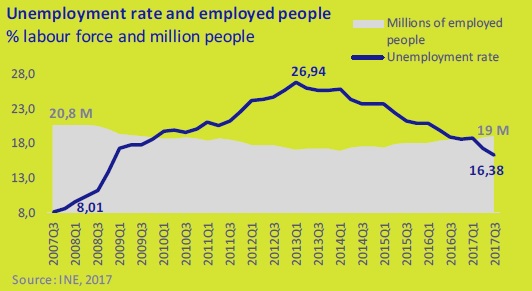

The number of unemployed people decreased by 589,100 people to 3,731,700. The unemployment rate stands at 16.38%.

Employment and unemployment in October (Ministry of Employment and Social Security)

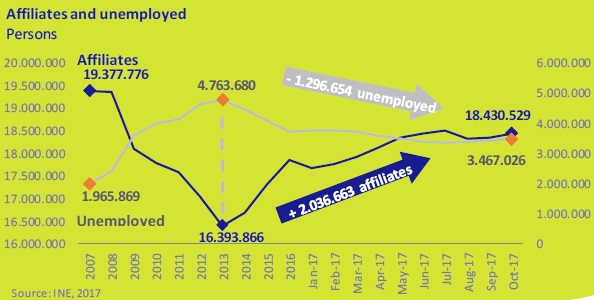

The number of contributors to the Social Security scheme reached 18,430,529 (▲ 3.46% year-on-year = 617,173 more contributors).

The registered unemployment rate decreased by 7.91% year-on-year (▼ 297,956 people) to 3,467,026, the lowest in 8 years. On a monthly basis, unemployment grew by 56,844 people, recording its biggest increase in Catalonia (▲ 14,698) and Andalusia (▲ 12,971).

EUROPE

GDP flash estimate Europe Q3 2017 (Eurostat)

In Q3 2017 GDP in both the EU28 and the Eurozone grew by 0.6% quarter-on-quarter (vs. 0.7% in Q2 2017) and by 2.5% year-on-year (vs. 2.4% and 2.3% respectively in Q2 2017).

Unemployment Eurozone, Sep. (Eurostat)

In September the number of unemployed in the Eurozone was 14.513 million, with the unemployment rate shrinking to 8.9% (vs. 9% in August and 9.9% a year earlier), its lowest since January 2009. Greece and Spain continue to have the highest unemployment rates vs. Germany and Malta that register full employment rates.

EMU monetary policy (ECB)

Between January and September 2018, the ECB will lower monthly purchases (QE) from €60,000m to €30,000m. This decision is justified by the confidence in the medium-term recovery of inflation in a favourable macroeconomic scenario.

However, interest rates will remain at current levels and the reinvestments in maturing assets on the ECB balance sheet will continue.

Eurozone government debt Q2 2017 (Eurostat)

In Q2 2017 the public debt in the Eurozone stood at 89.1% of GDP (vs. 90.8% in Q2 2016). By country, Greece, Italy and Portugal are at the head, while Estonia, Luxembourg and Lithuania have the lowest debt. In the last year, the debt level has been significantly reduced (> 4 pp of GDP) in Greece and the Netherlands, and increased (by about 1 pp) in France and Portugal.

The average public deficit in the Eurozone stood at 1.2% of GDP in Q2 2017, three points below that of Q2 2016.

United Kingdom (BoE)

The Bank of England, for the first time in a decade, has raised interest rates by 25 bp bringing them to 0.5%. This decision comes in a context of low unemployment and high inflation (3%), caused in part by the impact of Brexit.

The BoE anticipates possible further increases to bring inflation close to its target (2%).

However, it is keeping the asset purchase programme set at £10,000m a month.

INTERNATIONAL

Prices in Japan (BoJ)

In September, inflation in Japan increased again slightly to 0.7% (vs. 0.6% in August), although it is far from the target set by the BoJ (2%).

Core inflation (excluding fresh foods and energy) remained at 0.2%, which highlights the difficulties faced by the Japanese economy to control the risks of deflation.

Mexican economy

In Q3 2017, the Mexican economy grew by 1.7%, its lowest rate in three and a half years, due to:

• The earthquakes on the 7th and 19th of September,

• The hurricanes that hit the country,

• The drop in remittances (its 2nd largest foreign exchange earner) 1% year-on-year.

In quarterly terms, in comparison with Q2 2017, the economy shrank for the first time in 4 years (-0.2%).

It is anticipated, however, that activity will pick up, closing the year with an increase in GDP above 2%, in line with the IMF forecast in October (2.1%).