SPAIN

Employment January 2017 (Ministry of Employment and Social Security)

Registered unemployment rose by 57,257 persons from December to reach 3,760,231, one of the lowest levels of the past seven years. In year-on-year terms, the number of people without work dropped by 390,524 (down 9.41%), the largest decline since 1999.

In December there were 1,633,592 new contracts (up 16.94% year-on-year), of which 150,162 were permanent (9.2%). The average affiliation to Social Security was 17,674,175 persons, 174.880 fewer than the previous month but 569,817 more (up 3,33%) than in the same period of the previous year.

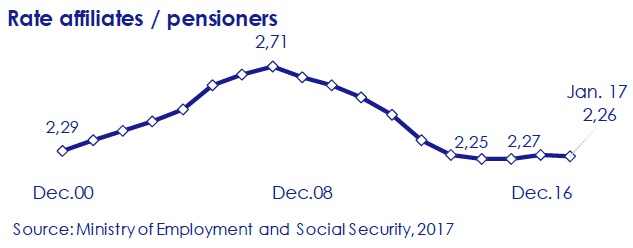

At present the ratio of affiliates to pensioners is 2.26.

CPI January 2017 (INE)

For the fifth consecutive month inflation reached 3% annually (vs. 1.6% in December), the highest rate since July of 2013 (1.8%), principally because of increases in the price of fuels (+16% annually) and energy (electricity: +26,2%).

The annual rate of underlying inflation increased by one decimal point, to 1.1%.

Public deficit (European Commission)

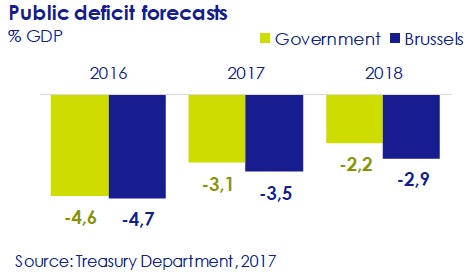

The European Commission has revised upward its prediction for Spain’s public deficit in 2017 to 3.5% of GDP (+2.2 billion euros), four decimal points above the objective of 3.1%), which would suggest an additional adjustments of 4.4 billion euros in the budget. In 2018, the deficit is expected to -2.9% of GDP.

Prediction for tax collection

For 2016, the Treasury Department predicts that tax revenues will reach 187.98 billion euros, some 5.54 billion less than what was budgeted (193.52 billion). With respect to 2015, classified by the kind of tax, income will increase 12.8% in the Corporation Tax, 3.6% in the VAT, 3.1% in Excise Duties and 0.4% in the Personal Income Tax.

In 2017, the year in which the authorities expect to recover the GDP level of 2007, it is estimated that there will be some total tax income of 202.593 billion, some 0.9% more than pre-crisis levels (200.676 billion).

EUROPE

GDP growth in the 4Q of 2016 (Eurostat)

GDP in the Eurozone grew 0.4% on a quarterly basis and 1.7% year-on-year (0.5% and 1.8% respectively in the EU28), driven by the still low energy prices, the depreciation of the euro against the dollar, and lower interest rates. Spain is among the countries that are growing the most, with a quarter-on-quarter rate of 0.7% and an annual rate of 3%.

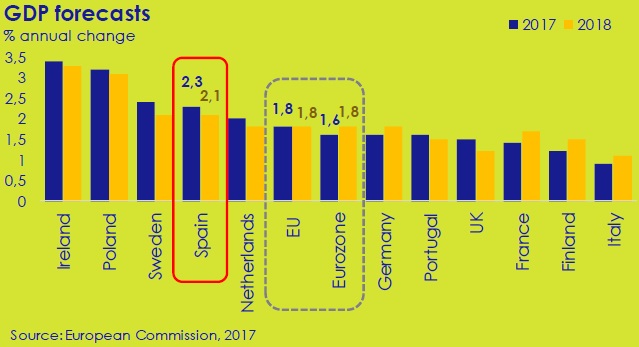

Winter predictions (European Commission)

The European Commission has revised upwards its predictions for the Eurozone, and is now forecasting annual GDP growth of 1.6% in 2017 and of 1.8% in 2018. In Spain there is expected to be an advance of 2.3% and 2.1%, respectively.

Private consumption will continue to be the main engine of growth, supported by improvements in employment and a rise in salaries, although the reduction in household purchasing power due to higher inflation will slow that growth.

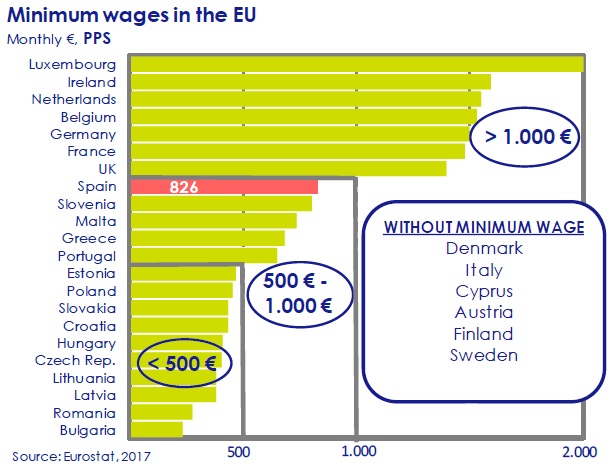

Minimum salary (Eurostat)

With the exception of Denmark, Italy, Cyprus, Austria, Finland and Sweden, the rest of the EU28 countries have a minimum salary set by law, divided into three categories depending on the quantity.

Expressed by Purchasing Power Standard (PPS), taking into account the price levels in each country, the differences in amount between them are notably reduced.

Germany. Overseas sector 2016

In 2016, German exports increased 1.2% yearon- year, to 1.2 trillion euros (38.5% of GDP), to reach a new record (Federal Office of Statistics). The exports to the Eurozone grew 1.8% (to 441.8 billion euros), while those to the rest of the EU countries did so by 2.8% (266.1 billion). By contrast, sales to non-EU countries dropped 0.2% (499.6 billion).

Imports totalled 954.6 billion (+0.6% year-onyear), surpassing the previous maximum, in 2015 (949.2 billion). The present trade surplus is 252.9 billion (vs. 244.3 billion in 2015), equivalent to 8.1% of the German GDP.

INTERNATIONAL

Japanese growth in the 4Q of 2016

The Japanese economy grew 1% year-on-year (vs. 1.2% in 2015) and 0.2% quarter-on-quarter (the fourth consecutive rise since September of 2013), driven by company investment (0.9% quarter-on-quarter) and by exports (2.6%), which improved because of greater demand from China and the United States and because of the weakness of the yen (since November it has lost 8.5% of its values against the dollar.)